A 2026 E-Bike Buyer's Guide to the Best eBIKE INSURANCE

A 2026 E-Bike Buyer's Guide to the Best eBIKE INSURANCE

BikeInsure, a licensed insurance producer specializing in bicycle and eBike insurance across the United States, has released A 2026 E-Bike Buyer's Guide to the Best eBIKE INSURANCE. The guide answers the questions every electric bike owner is searching for in 2026: whether homeowners or auto insurance covers an eBike, what standalone eBike insurance actually protects, and how to choose the right policy as eBike theft climbs.

Quick answer: No, homeowners and auto insurance do not cover your electric bike. Yes, your eBike needs its own standalone policy. BikeInsure offers nationwide eBike coverage for riding accidents, transit, and theft, with a low deductible and claims that won't affect your other insurance policies. Get a Quote.

Buzzy Cohn, CEO of BikeInsure, shared: "Every electric bike owner is weighing the same thing — they've made a real investment, and they want to protect it against the two things that hurt most: an unexpected riding accident and theft. Theft is the worst case, because a stolen eBike is a total financial loss. If a cycling accident damages a derailleur, the repair is manageable. If a $4,000 eBike is stolen, it's gone."

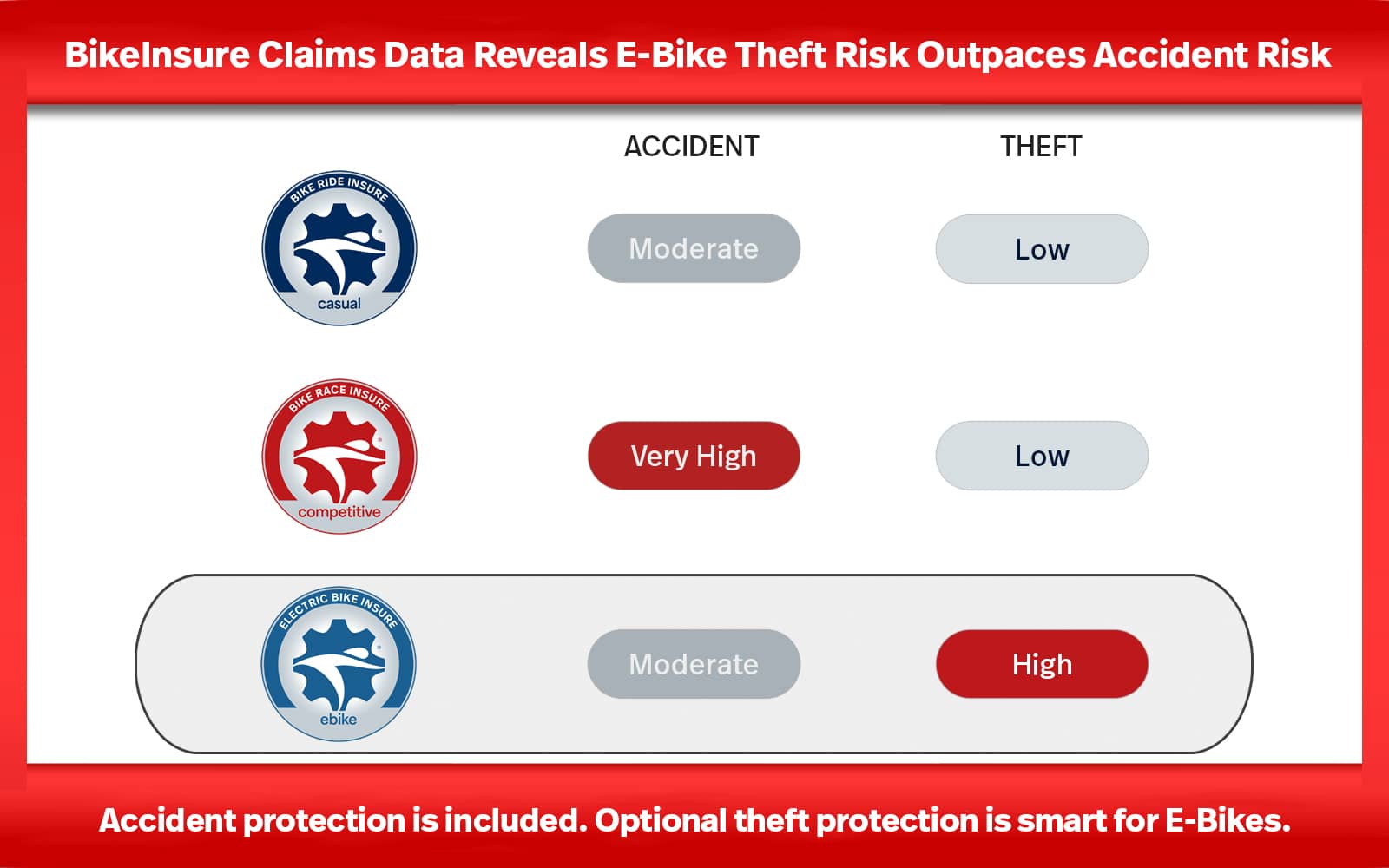

"Across BikeInsure's overall program, approximately 80% of claims have involved riding accidents and about 20% theft — which is exactly why we offer theft as optional coverage. The electric bike is the exception. An eBike is stolen far more often than a non-electric bike, and it's the only category in which theft outpaces accidents. For an eBike, theft protection isn't a nice-to-have; it's an essential layer of protection that delivers real peace of mind."

Does homeowners insurance cover an electric bike?

No. Homeowners insurance is insurance for a home — not for an eBike.

Homeowners policies typically classify electric bikes as motorized vehicles and exclude them from personal property (Coverage C / Contents) coverage. Even a scheduled personal property rider — the kind used for jewelry, art, or firearms — generally will not cover an eBike, because the motorized-vehicle exclusion applies.

Auto insurers, including State Farm, Allstate, Farmers, and USAA, also exclude eBikes, defining "insured autos" and "cars" as four-wheeled private passenger motor vehicles.

What does filing a homeowners insurance claim cost you?

Because eBikes are categorized as motorized vehicles, a home policy will simply deny a claim for an eBike loss — there is nothing to file. But there is a broader reason never to route any bike loss through your homeowners coverage. Insurance experts treat home insurance as protection against major losses to the home itself, and filing claims of any kind carries real consequences:

- Premium increase. After a qualified homeowners or renters claim, premiums often rise at renewal — frequently 25% to 60%, depending on your state.

- Non-renewal. Insurers may decline to renew (cancel) a policy after multiple claims within three years, even with a perfect payment history.

- CLUE report entry. Claims are recorded in the Comprehensive Loss Underwriting Exchange (CLUE) database, which insurers use to underwrite and rate future policies. That record can make coverage harder and costlier to obtain.

The smarter alternative protects your home policy. The best feature of a BikeInsure policy is that filing an eBike claim won't affect your other insurance policies. Your homeowners coverage stays in good standing — a true WIN-WIN. See the top benefits of bike insurance for homeowners.

A California ARI eBike owner shared their homeowners exclusion: "I went through my Allstate homeowners policy for bike coverage with my agent and discovered it doesn't protect my bike from theft away from my residence. We looked further and found the policy excludes eBikes outright — 'Property we do not cover' lists 'motorized land vehicles, including any land vehicle powered or assisted by a motor or engine.' BikeInsure is the ideal eBike insurance solution."

Do you need separate insurance for an electric bike?

Yes. Because homeowners and auto policies exclude eBikes, a standalone eBike policy is the only reliable way to fully protect your investment — including non-stock accessories and components.

BikeInsure is a cost-effective, standalone insurance solution built specifically for electric bikes. Signing up takes about two minutes, coverage is available nationwide, and the policy applies to eBikes that meet the 3-Class eBike standard, which limits the maximum pedal-assist speed of 28 mph.

What does eBike insurance cover?

BikeInsure offers comprehensive protection across the three ways eBikes most often suffer a loss — riding accidents, transit, and theft — plus the accessories that make an eBike yours. Coverage applies to eligible electric bikes that meet the 3-Class eBike standard (a 28 mph pedal-assist maximum). It does not extend to non-eligible vehicles such as electric motorcycles, mopeds, scooters, or other motorized vehicles that fall outside those classes.

eBike accident damage coverage

BikeInsure insures against sudden and accidental direct physical loss to your insured new or used eBike. It reimburses repairs to your eBike and listed accessories from riding and transit accidents, subject to a low per-occurrence deductible.

A Trek electric hybrid riding accident claim: An Omaha, Nebraska rider enrolled a Trek Verve+ 4S eBike with BikeInsure. Less than three months later, a riding accident damaged the brake handles, brake rotors, and front wheel. After filing, the customer received a $291 check covering OEM parts, labor, and tax at the local bike shop of their choice.

eBike transit damage coverage

Standard BikeInsure transit coverage protects your insured eBike during secure transport by car, bus, or train on land, by ship over water, and by airplane — within the United States, its territories (such as Puerto Rico), and Canada.

A Pivot e-mountain bike transit claim: A Utah resident enrolled a Pivot Shuttle eBike with bar grips, pedals, and a helmet listed as accessories. While stopped at a traffic light, an unlicensed driver struck the rear of the insured's SUV, causing the eBike secured to the rear rack to be destroyed. BikeInsure paid $10,000 for the eBike; the customer paid only a low deductible.

eBike theft protection

BikeInsure gives eBike owners a choice other insurers don't: customers select theft protection together with damage coverage, or choose damage-only coverage for their eBike. When optional theft is selected, the policy protects the covered equipment against the financial loss of theft, subject to a low deductible.

BikeInsure provides one of the broadest definitions of bicycle theft

BikeInsure covers "secured property" — and that one phrase changes everything at claim time. With BikeInsure, your eBike must be secured when left unattended, but there is no requirement to lock it to an immovable object, and no required lock type.

Other bike insurance policies impose far narrower theft requirements:

Markel (and Velosurance, which it underwrites) won't pay a theft claim away from home unless the bike was "secured to an immovable object with an appropriate security locking device" — and its policy defines an immovable object as something fixed in concrete or stone that can't be undone, removed, or lifted.

Sundays is the narrowest: the bike must be locked through the frame to an immovable object with an approved lock that is hardened steel, purchased within the last two years, and priced above a minimum.

A Tern e-cargo bike owner shared their theft claim: "We felt BikeInsure provided better value when we switched from Markel. The crucial difference was the theft language. Markel required the bike be 'secured to an immovable object,' while BikeInsure covers secured property — which worked in our favor. The claims process was efficient and supportive; I replaced the bike at my favorite shop. The replacement totaled $5,417 for a 2024 Tern GSD Gen2 — and we only paid a small theft deductible rather than the full amount."

A Gazelle eBike owner shared their theft claim: "Standing at the hospital bike rack where my eBike was stolen, I called BikeInsure. They answered immediately and guided me through filing, starting with a police report. The settlement was a breeze — they offered me a check or direct payment to the shop, and I chose the shop. I picked up my new Gazelle eBike, and my only cost was the small BikeInsure deductible."

eBike accessories and components coverage

Accessories and components listed on your policy are included in your eBike's overall insured value. Many riders don't realize how much value rides on top of the frame.

- Accessories include bags, bottle cages, cameras, computers, lights, mounted pumps, and radar. (Quality panniers like Ortlieb can run well over a hundred dollars apiece.)

- Components include the groupset (gruppo), pedals, power meter, saddle, and wheelset.

Non-stock attached accessories and components listed at enrollment — or added later via policy endorsement — are covered and included in the eBike's value. BikeInsure is the official eBike insurance provider for The New Wheel Electric Bike Shops in California, where many customers list their Tern ebike accessories and Ortlieb panniers directly on their policies.

Why eBike insurance matters more in 2026

Why is eBike theft rising in 2026?

Theft data from the National Insurance Crime Bureau (NICB) and Bike Index point to a sharp year-over-year rise in eBike theft reports heading into 2026, with major US cities among the hardest hit. The reasons are simple: eBikes hold high resale value, their batteries and motors are sold for parts, and their weight pushes thieves to cut locks and roll them away. For owners, a stolen eBike is a complete financial loss — exactly the scenario standalone theft protection is built for.

That is why a standalone policy built specifically for eBike equipment and theft has become essential. BikeInsure protects the two losses that hit eBike owners hardest — accidental physical damage to the bike and theft — with a low deductible and claims that won't affect your other insurance policies.

How to Choose the Best eBike Insurance

When comparing eBike insurance, look past the headline and read how each policy actually pays. A handful of details separate a policy that protects your eBike from one that mostly protects the insurer:

- Standalone. Your eBike should be covered on its own, without ever touching your homeowners or auto policy — so a claim never raises your home premium or lands on your CLUE report. BikeInsure is standalone by design.

- Riding accident, transit, and theft. Confirm all three are available, and that theft can be selected for your eBike. BikeInsure offers all three, with theft as an option you control.

- Broad theft language — read the lock clause. This is where policies quietly diverge, and the fine print gets strict fast. Markel and Velosurance, for example, won't pay a theft claim away from home unless the bike was "secured to an immovable object." Sundays goes further still, requiring it be locked through the frame to an immovable object with an approved lock that is hardened steel, purchased within the last two years, and priced above a minimum. BikeInsure covers "secured property" — your eBike simply needs to be secured when unattended, with no immovable-object requirement and no required lock type. At claim time, that one clause is the difference between a paid claim and a denied one.

- Carbon frames: replaced, not patched. When a carbon frame is damaged, the question that matters most is whether your insurer replaces it or repairs it — and the cheaper path for the insurer is repair. Velosurance (underwritten by Markel) publishes a blog post, "Carbon fiber bicycle frames — repair or replace?", favoring carbon repair, and a Velosurance FAQ concedes a repair facility "cannot guarantee that the frame will retain the manufacturer's warranty." Most bicycle manufacturers warn that repairing a carbon frame can void its warranty. We handle claims differently than Velosurance and Markel do. To date, every BikeInsure claim for a carbon frame cracked in a covered accident has been settled with a new OEM frame replacement — so you ride away on a frame that's new, warrantied, and whole, not patched.

- Fast, personal claims that pay your way. A policy is only as good as the day you file. BikeInsure handles claims quickly and personally — you file your claim through our customer portal, then choose a check or direct payment to the bike shop of your choice. 40% of BikeInsure claims have been resolved in under seven days, some in as little as a single day.

- Accessories and components counted. Bags, lights, wheelsets, power meters — confirm they can be listed and valued rather than left off. BikeInsure includes listed accessories and components in your eBike's insured value.

- Low, predictable deductible. A low per-occurrence deductible keeps repairs and replacements simple — no surprise math at claim time.

- A+ rated carrier, nationwide. Coverage is only as strong as the company behind it. BikeInsure is underwritten by Great American Insurance Company — rated "A+" (Superior) by AM Best — with protection that follows your eBike across the country and into Canada.

Comparing providers? See how BikeInsure stacks up against Velosurance, Markel, and Sundays, or review the full comparison page.

How much does eBike insurance cost?

eBike insurance is more affordable than most riders expect — and far less than the cost of replacing a stolen or wrecked electric bike out of pocket. BikeInsure pricing reflects your eBike's value and the coverage you select, and monthly plans include a small Installment Processing amount as part of the payment. BikeInsure annual policies for electric bikes start at approximately $16 per month for accidental damage coverage, or about $20 per month with optional theft protection added — each with a flat $150 deductible. The fastest way to see your exact coverage and price is a quote. Get a Quote.

Who is behind BikeInsure?

BikeInsure offers affordable, comprehensive insurance for bicycles and eBikes across the United States. As a licensed insurance producer, BikeInsure is the official bike insurance partner of USA Cycling, the International Mountain Bicycling Association (IMBA), USA Triathlon, the League of American Bicyclists, and the Adventure Cycling Association.

The plan is underwritten by Great American Insurance Company, rated "A+" (Superior) by AM Best, an authorized insurer in all 50 states and Washington, D.C. For over 150 years, Americans have trusted Great American Insurance Company for best-in-class protection and service.

Signing up takes just two minutes. Get BikeInsure and enjoy the ride!

eBike Insurance FAQ

Does homeowners insurance cover an electric bike? No. Homeowners policies generally classify eBikes as motorized vehicles and exclude them, and a scheduled rider typically won't help.

Does auto insurance cover an eBike? No. Auto insurers define covered vehicles as four-wheeled passenger cars and exclude eBikes.

Do you need separate insurance for an eBike? Yes. A standalone eBike policy is the only reliable way to protect against riding accidents, transit damage, and theft without affecting your other policies.

Is eBike theft covered by insurance? Yes, when theft protection is selected with BikeInsure. Coverage uses a broad "secured property" definition, subject to a low deductible.

Are eBikes stolen more often than regular bikes? Yes. Industry theft data show that eBikes are targeted at a higher rate, driven by their resale value and demand for batteries and parts.

Will filing an eBike claim raise my home insurance? No. A BikeInsure claim won't affect your homeowners or other insurance policies.

What does eBike insurance cost? Pricing depends on your eBike's value and the coverage you select. Get a Quote to see your exact price in seconds — and enroll in about two minutes.

Got eBike insurance questions? Ask Buzzy.

Still have a question the guide didn't answer? Ask Buzzy, our AI assistant. Buzzy answers coverage, claims, and eligibility questions in plain language — any time, in your language, with guidance tailored to where you ride.

Try asking: "Is my Class 3 eBike eligible?" · "What does theft protection include?" · "How fast are claims paid?"

Ready for eBike insurance?

Casual Riding — No racing license required. United States + Canada territory.

Competitive Racing — Casual riding + racing events. Worldwide coverage territory.

Electric Bikes — Up to 28 mph. United States + Canada territory.

Ride Covered LLC dba BikeInsure is a licensed insurance producer offering affordable bicycle and eBike coverage nationwide in the United States, underwritten by Great American Insurance Company, rated "A+" (Superior) by AM Best, and an authorized insurer in all 50 states and D.C. The coverage description is summarized; refer to the actual policy for full terms, conditions, limits, and exclusions.