Warning: Homeowners Insurance is NOT for Bicycles or eBikes!

Homeowners Insurance is Coverage for a Home, NOT a Bicycle or eBike

The financial loss of a bike, e-bike, or para-adaptive cycle due to a riding or transit accident or theft should be a routine insurance claim.

HomeInsuranceProblem.com will explain why homeowner's insurance should NOT be used to cover a bike or e-bike!

It's important to consider the consequences of filing a home insurance claim. After a 'qualified' homeowners or renters insurance claim, you may encounter several costs, including an increase in your premiums, the possibility of your policy not being renewed, and an entry in the Comprehensive Loss Underwriting Exchange (CLUE) report. This record can make it costly and difficult to obtain insurance from private insurers in the future.

Insurance experts recommend homeowners view home insurance as protection against significant losses rather than as coverage for items like bicycles, even with a "Scheduled Insurance Rider."

Why risk losing a homeowner's insurance policy when there's a smart alternative that can insure bicycles, ebikes, and adaptive cycles like BikeInsure? One of the best features of a BikeInsure policy is that if you ever need to file a claim, it won't affect your other insurance policies. This means your homeowner's policy will remain in good standing. So it's a true WIN-WIN cycling situation — you can fully protect your bike with BikeInsure while keeping your homeowner's insurance intact!

Leanda Cave's Homeowner Insurance Story

"I have known BikeInsure for many years and initially spoke with CEO Buzzy Cohn when he developed the bike insurance product in response to an expensive bicycle accident he experienced," said Leanda Cave. "At that time, I had just received a Home Insurance Cancellation notice labeled 'Homeowners Insurance Notice of Non-Renewal. YOUR INSURANCE COVERAGE WILL TERMINATE.' I had two home insurance claims, one was a minor water leak that damaged a floor in my Florida condominium, and the other was bike related. Although my homeowner's insurance seemed effective at first because I received the necessary checks for the damages, it was later canceled, which made it challenging to find alternative homeowner's insurance. When I learned that BikeInsure offered a separate bike insurance policy from homeowner's specifically to insure bicycle equipment, that would not affect my homeowner's policy in the event of a claim, I realized BikeInsure had a simple solution for insuring all valued bikes across the United States."

Why Homeowners' Insurance should only be used for Significant Home Losses

- TheZebra.com - "While having insurance protection on your property is vital, it works like a double-edged sword — the more you involve your home insurance company, the more expensive your rate will be for the foreseeable future. Therefore, it is crucial to understand which situations are worth filing homeowners claims for and which aren't."

- Bankrate.com - "Homeowners insurance rates often increase after a claim because it leads your insurance company to believe that you are more likely to file another claim in the future. This is especially true for water damage, dog bites, and theft claims. To compensate for another potential claim payout, the property insurer proactively raises your premium."

- Insure.com - "Home insurance premiums increase on average by 27% after one theft claim."

- The Washington Post - Why your homeowner's insurance probably wasn't renewed. "Insurance companies focus on the most recent three years of loss history, which is documented in a Comprehensive Loss Underwriting Exchange (CLUE) report."

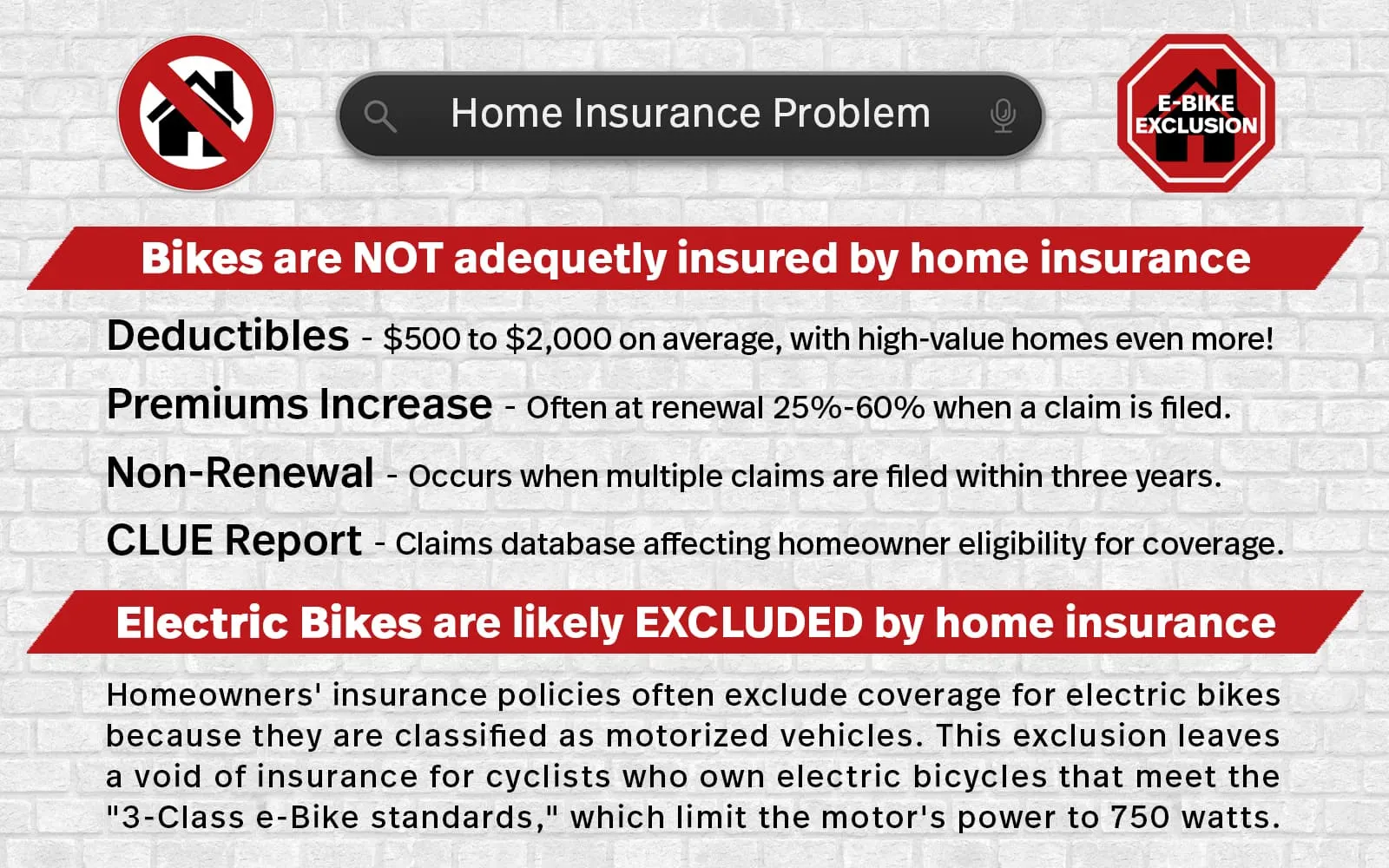

The top 4 reasons why Home Insurance should NOT cover a bike.

- Deductible: A standard homeowner's insurance deductible is usually $500 to $2,500, according to PolicyGenius.com. Although, deductibles for higher-valued homes are sometimes $5,000 or more, according to USnews.com.

- Premium Increase: When a homeowner's claim is processed, often the result is a 25% - 60% increase in insurance premium at policy renewal.

- Non-Renewal: Homeowners' insurance companies may have to non-renew a policy if multiple claims are filed within three years.

- CLUE Report: The Comprehensive Loss Underwriting Exchange is a claims history database by LexisNexis. This report records every homeowner's insurance claim, allowing insurance companies to access consumer claims information when underwriting or pricing an insurance policy. Additionally, insurers use the CLUE Report to help determine eligibility for insurance coverage.

Farmers Homeowner Insurance Customer Story

"My wife had a bike accident, leaving her Trek Domane bicycle with a cracked carbon frame. We live in California, where several Insurance Carriers have stopped selling new home insurance policies. As a result, although our Farmers insurance may have covered the claim, we realized that doing so, as our agent agreed, could cancel our homeowner's insurance policy. Therefore, we paid out-of-pocket to replace my wife's bicycle and decided to get a separate bike insurance policy for both of our bicycles. We confidently chose BikeInsure because it is the only bicycle insurance company endorsed by USA Cycling.

We love cycling. We don't golf. We ride. Riding bikes together is an activity that we thoroughly enjoy. However, accidents can happen, and they can be expensive. Our lesson learned was our homeowner's insurance policy could not cover our bikes, and that realization cost us a lot of money. Even with Trek's Crash Replacement Program, we purchased the new bike for a 20% discount. However, with the BikeInsure policy covering the new Trek bicycle, we will only pay the accident deductible if my wife has that same accident. With BikeInsure, my wife can enjoy her Trek bike with peace of mind, knowing that we won't have to spend nearly $7,000 for a replacement should an accident happen.

We ordered a new bike from the Project One department with a custom tie-dye paint scheme. Once we received it, we insured it with BikeInsure to protect ourselves from future financial burdens. Now, if any accident happens, we'll only have to pay an accident deductible instead of the thousands it costs to replace a nice bike. We found the right bike insurance solution with BikeInsure through USA Cycling. Now, our bicycles are insured, and our homeowner's insurance will remain unaffected by our bikes."

Electric Bikes have No Homeowners Insurance

Homeowners insurance personal property is generally referred to as Coverage C or Contents Coverage. A Scheduled Insurance Rider is an optional endorsement or add-on to a standard homeowners insurance policy that provides additional coverage for specific high-value items. It's designed to cover items like jewelry, art, collectibles, or firearms, which may not be fully covered under a standard policy's personal property limits.

Homeowners' insurance policies exclude ebikes as the homeowner's property is not covered because ebikes are classified as motorized vehicles.

The smart solution is a separate ebike insurance policy which is an essential need for every ebike cyclist, providing 'peace of mind' financial protection for their valued electric bike against accidents and theft risks.

The Must-See Video Cyclists Can't Afford to Miss

America's Best E-Bike Insurance, BikeInsure, fills the gap by ensuring cyclists' ebikes are financially protected against riding, transit, and theft risks. The comprehensive ebike insurance solution is available nationwide. It features a low deductible, allowing cyclists to easily get their ebikes repaired or replaced, which provides significant reassurance for their investment in an electric bike. Additionally, filing an ebike claim with a BikeInsure policy will not impact your other insurance policies. This coverage applies to ebikes that meet the "3-Class ebike standards," which restrict the motor power to 750 watts.

Homeowners Insurance E-Bike Exclusion Story

"I had a difficult time finding insurance that would cover my E-Bike. I thought my homeowners would cover any loss or theft, but to my surprise, they deny all ebike coverage.

At the beginning of my search, I found other online bike-specific insurance too costly. Then, I came across BikeInsure and decided to give them a call. I spoke with the BikeInsure CEO for quite some time. He was very helpful in explaining to me in great detail the ins and outs of insurance, especially for bicycles. The process was simple, and I found the amount of coverage and the monthly cost to be of good value. I feel secure knowing I have a great policy to protect my much-loved E-bike!

Thanks, BikeInsure, for providing a great product!"

Allstate Homeowners Insurance E-Bike Exclusion Story

"I went through my Allstate Homeowners Insurance Policy for bike coverage in California with my insurance agent. I discovered that it does not protect the theft of my bicycle if it gets stolen away from my residence.

We looked further into the Allstate coverage of an electric bike because I own a Mountain eBike, and we found the Allstate policy excludes eBikes, "Property we do not cover" is "Motorized land vehicles, including, but not limited to, any land vehicle powered or assisted by a motor or engine."

BikeInsure is the ideal eBike insurance solution."

BikeInsure makes BIKE INSURANCE more affordable and accessible for bike, e-bike, and para-adaptive cycle owners in the United States. Bicycle owners need to obtain separate insurance for comprehensive protection of their investment and all valued non-stock attached accessories.

Bike Accident Damage Coverage

BikeInsure insures against the risk of sudden and accidental direct physical loss to insured new or used bike, e-bike, and para-adaptive cycle equipment. It reimburses your enrolled bicycle's repairs and listed accessories due to riding and transit accidents.

BikeInsure physical damage coverage has an accident per occurrence deductible.

Bike Transit Damage Coverage

The standard BikeInsure Transit Coverage includes the secure transportation of your insured bike, e-bike, or para-adaptive cycle via car, bus, or train on land, as well as by ship over water and by airplane to your preferred destination. This coverage applies within the United States, its territories (such as Puerto Rico), and Canada.

Bike Theft Protection

BikeInsure offers a unique choice compared to other bike insurance providers for Bike Theft Protection from and away from home. BikeInsure allows customers to pay for theft protection with bike damage coverage or select bicycle damage coverage only for an enrolled bike, e-bike, or para-adaptive cycle. When optional theft is selected, the policy protects the covered equipment against the financial risk of theft.

In the event of bike theft loss, you are responsible for a theft deductible.

BikeInsure provides the broadest definition of bicycle theft and includes language regarding bicycle theft as 'secured property'.

In contrast, another bike insurance policy offers narrower coverage, stating that the bike must be "secured to an immovable object with an appropriate security locking device."

Another bike insurance company has the narrowest requirement, specifying that the bicycle "must be locked by an approved lock to an immovable object."

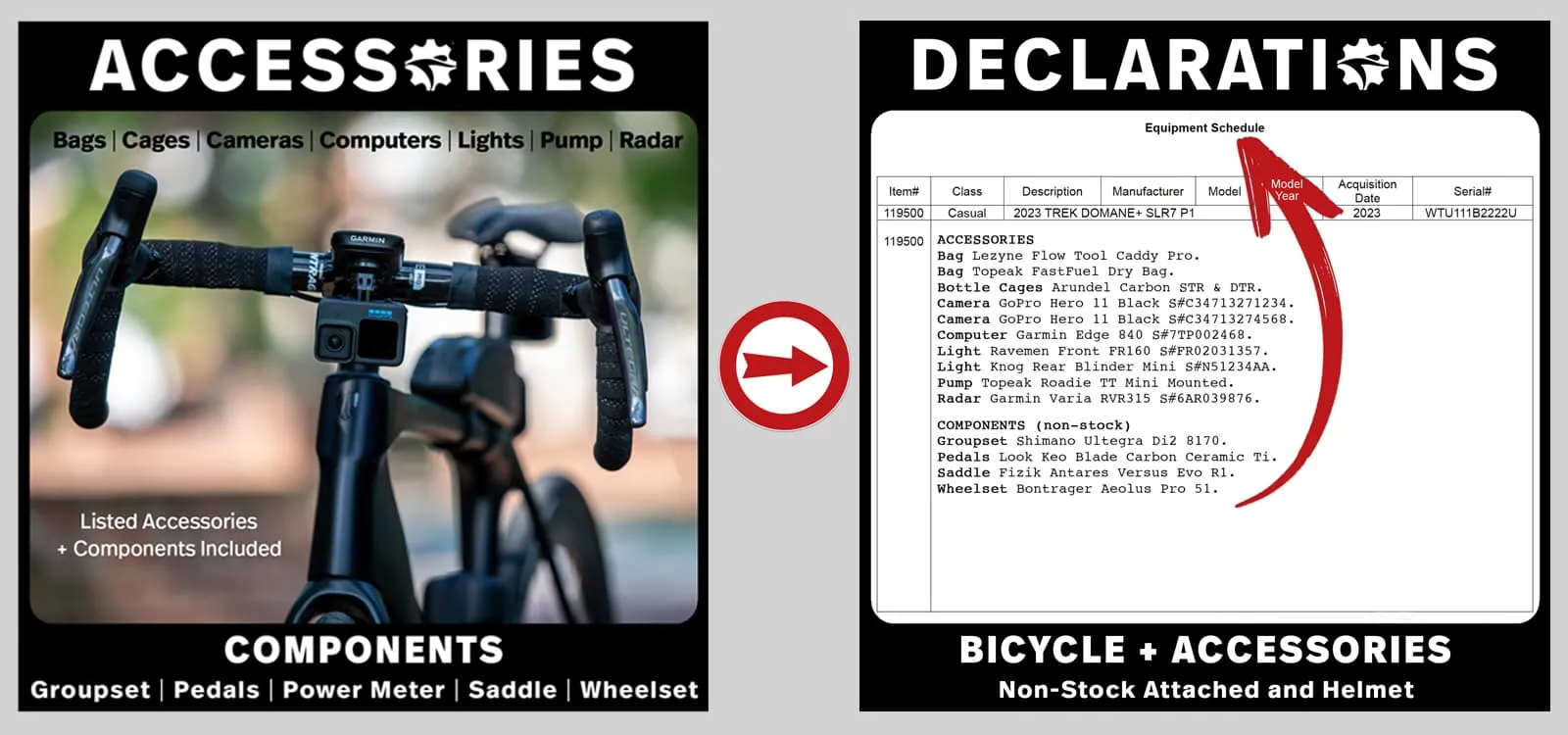

Bike Accessories Included

Non-stock-attached bike accessories and components that are listed at enrollment or added to the policy via future policy endorsement requests will be covered and included in the bike's overall value.

Accessories include items such as bags, bottle cages, cameras, computers, lights, mounted pumps, and radar. Whereas, Components include, but are not limited to, the groupset (gruppo), pedals, power meter, saddle, and wheelset.

In addition to BikeInsure covering each non-stock-attached bike accessory and component that is listed at enrollment or added to the policy via future policy endorsement requests, a bicycle helmet is also an accessory that is covered when listed. This $300 KASK Protone Bike Helmet was cracked in the crash and part of a BikeInsure claim settlement.

BikeInsure Claims

A separate bike insurance policy with BikeInsure helps reduce the financial risks associated with unexpected accident occurrences of riding, transit, and theft that all bicycle and e-bike owners face in the United States. Bicycles and e-bikes require separate bike insurance to cover these risks.

Filing a claim with BikeInsure will not impact your other insurance policies.

Specialized Road Bike Accident Claim

"I signed up for bike insurance with BikeInsure in February 2023, so I've had coverage for a few years. I hit a bump riding through Golden Gate Park in San Francisco and went down hard. Luckily, I wasn't hurt, but my bike took a serious hit—cracked top tube, seatstay, destroying my shifters, and even my helmet. It was rough. Thankfully, Bikeinsure made the whole process super smooth. They were responsive and helpful, and I received a payout of $8,266 by check just 9 days later. The coverage is surprisingly affordable and backed by a reputable insurer, which gives me peace of mind.

I was grateful that the BikeInsure claim process was very simple. I crashed on January 9, 2025, filed the claim at BikeInsure.com on January 13th, and the bike insurance check for $8,266 was paid 9 days later. My responsibility was limited to the BikeInsure accident deductible. BikeInsure also covered my $300 KASK Protone Bike Helmet, which was cracked in the crash!

I have consistently told every bike owner I know that BikeInsure is the most trustworthy bike insurance available. My friends even joke that I must be working for the company! I've since replaced my bike, and insured the new one with BikeInsure too. It's just good to know that if anything happens again, my bike is covered."

"We are incredibly grateful to have had bike insurance and not just any insurance — but specifically BikeInsure. We felt it provided better value when we switched from Markel to BikeInsure. One crucial factor we never thought would impact us was theft. Markel's policy stated that the bike must be "secured to an immovable object with an appropriate security locking device." In contrast, BikeInsure's policy specifies secured property, which worked in our favor.

Had we still been covered by Markel, I suspect our theft claim would have been denied. Fortunately, with BikeInsure, the claims process was efficient and supportive. I was able to facilitate the replacement at my favorite bike shop, Current eBikes, in California. The receipt for the replacement totaled $5,417 for the 2024 TERN GSD Gen2 in Satin Black. It was hard to believe that our e-bike was stolen, but thankfully, with BikeInsure, we only had to pay a theft deductible rather than the full $5,417!"

BikeInsure offers affordable and comprehensive insurance for bicycles and eBikes in the United States. Licensed insurance producer BikeInsure, the official bike insurance partner of USA Cycling, International Mountain Bicycling Association (IMBA), USA Triathlon, The League of American Bicyclists, and Adventure Cycling Association, is administering the insurance plan, underwritten by carrier Great American Insurance Company, rated "A+" (Superior) by AM Best, an authorized insurer in all 50 states and Washington, DC. For over 150 years, Americans have trusted Great American Insurance Company to protect them and render best-in-class service.

Signing up for BikeInsure is easy and takes just two minutes. So, Get BikeInsure and enjoy the ride!