Is Bicycle & eBike Insurance an Essential NEED? Yes! BRAIN Writes.

Is Bicycle & eBike Insurance an Essential NEED? Yes!

Washington (BRAIN) – A version of this article was published in both the November print and online Bicycle Retailer and Industry News editions.

BikeInsure aims to reduce cyclists’ homeowner’s insurance burden.

Buzzy Cohn had enough to deal with immediately following a bike crash from hitting a hubcap in the roadway during a group ride in 2012 that he didn't need more painful news.

His Trek Madone was destroyed and to replace it through homeowner’s insurance would have exposed his policy to cancellation. In the aftermath of the crash, Cohn knew what he had to do and it led him to eventually creating BikeInsure nearly three years ago, writing policies specifically designed to cover bikes and e-bikes.

With the price of components, not to mention bikes, on the rise, Cohn notes his company also can ease the pain of replacing damaged parts. So if you side-swipe that $250 Shimano XTR derailleur against a rock or snap that $450 SRAM eTap AXS shifter on the pavement, it’s not necessarily an “Oh, shift!” moment.

Cohn is developing partnerships with bicycle brands and retailers. In March, it announced it would be digitally integrated with SmartEtailing, now rebranded as Workstand, with more than 1,100 locally owned retailers on the platform.

“I couldn't imagine how an accident could cost so much money and possibly prevent me from continuing the simple joy of riding my bicycle,” Cohn said. “Unfortunately, the homeowner's insurance route had a large deductible.”

Cohn first acted on his homeowner’s insurance company’s recommendation to secure a separate policy for his bike because making bike-related claims could lead to cancellation of a homeowner’s policy. He found one provider but the application process was time-consuming with varying pricing, he said. For example, living in California raised the premium 32% higher than say in Wisconsin; an e-bike would raise it 30%; identifying as “commuter” raised the premium 10% higher than “casual” and “competitive” bike usage raised it 60%.

“Even when selecting carbon as bike material, it would also raise rates by 10%,” Cohn said. “The traditional bike insurance pricing model was similar to auto insurance. Shockingly, the final quote for my bicycle insurance premium was almost as expensive as the insurance premium I paid for my car.”

BikeInsure is underwritten by Great American Insurance Company and its plan has coverage up to $10,000 per bike — new and existing bikes — with a $100 deductible, and a fixed premium of $16.99 monthly nationwide. Coverage includes accidents on the bike — including in competition — and for transporting by land or air.

It also covers accessories like attached computers and cameras. Theft coverage is also available for an additional $8 monthly and includes a $10,000 annual claim limit and a $250 per occurrence deductible. Cohn said enrolling is a “two-minute process” at the BikeInsure website.

When filing an accident claim, it is necessary to provide a written estimate from an authorized bike shop, and having them perform the repair work is recommended.

BikeInsure also is the official bike insurance partner of USA Cycling. Last week, BikeInsure announced a partnership with IMBA.

“It became clear that there was a need for a better insurance product to cover cyclists' bikes without jeopardizing their homeowner's insurance policy,” said Cohn, whose background includes 28 years in e-commerce sales before creating BikeInsure.

When it comes to the three classes of e-bikes, BikeInsure covers them at no additional cost as long as they meet a state’s e-bike definition. Cohn said current underwriting restrictions don’t restrict battery fire risk. If a state does not define “e-bike,” BikeInsure will have it defined by federal law. About 20% of the bikes covered by BikeInsure are e-bikes.

Cohn noted that home insurance policies, for example, Allstate Insurance Company Deluxe Plus Homeowners Policy, often have specific language excluding e-bikes. Under "Property We Don't Cover: Motorized land vehicles, including but not limited to any land vehicle powered or assisted by a motor or engine. We do not cover any motorized land vehicle parts, equipment, or accessories attached to or located in or upon any motorized land vehicle."

Allstate does cover motorized vehicles to assist the handicapped.

"Electric bicycles are classified as motorized land vehicles — powered or assisted by a motor or engine — rather than personal property,” Cohn said. “Therefore, e-bikes are usually a homeowners, renters, and auto insurance exclusion. Since an e-bike often has no insurance by default upon purchase, the owner has substantial financial exposure for riding, transit, and theft risks of an electric bike until it has separate bike insurance.”

As with non-electric bikes, BikeInsure e-bike policies include reimbursement for repairs, listed accessories due to accidental damage when riding, and coverage during transit and extends to theft, if the optional $8 monthly insurance coverage is added.

BikeInsure doesn’t require e-bikes to be certified by a national testing lab — like UL — to be eligible for coverage.

“It is important to note that the cheaper brand of less-expensive electric bicycles that have experienced fire issues are not the type of e-bikes that have enrolled for BikeInsure, desiring comprehensive coverage of their e-bike,” Cohn said.

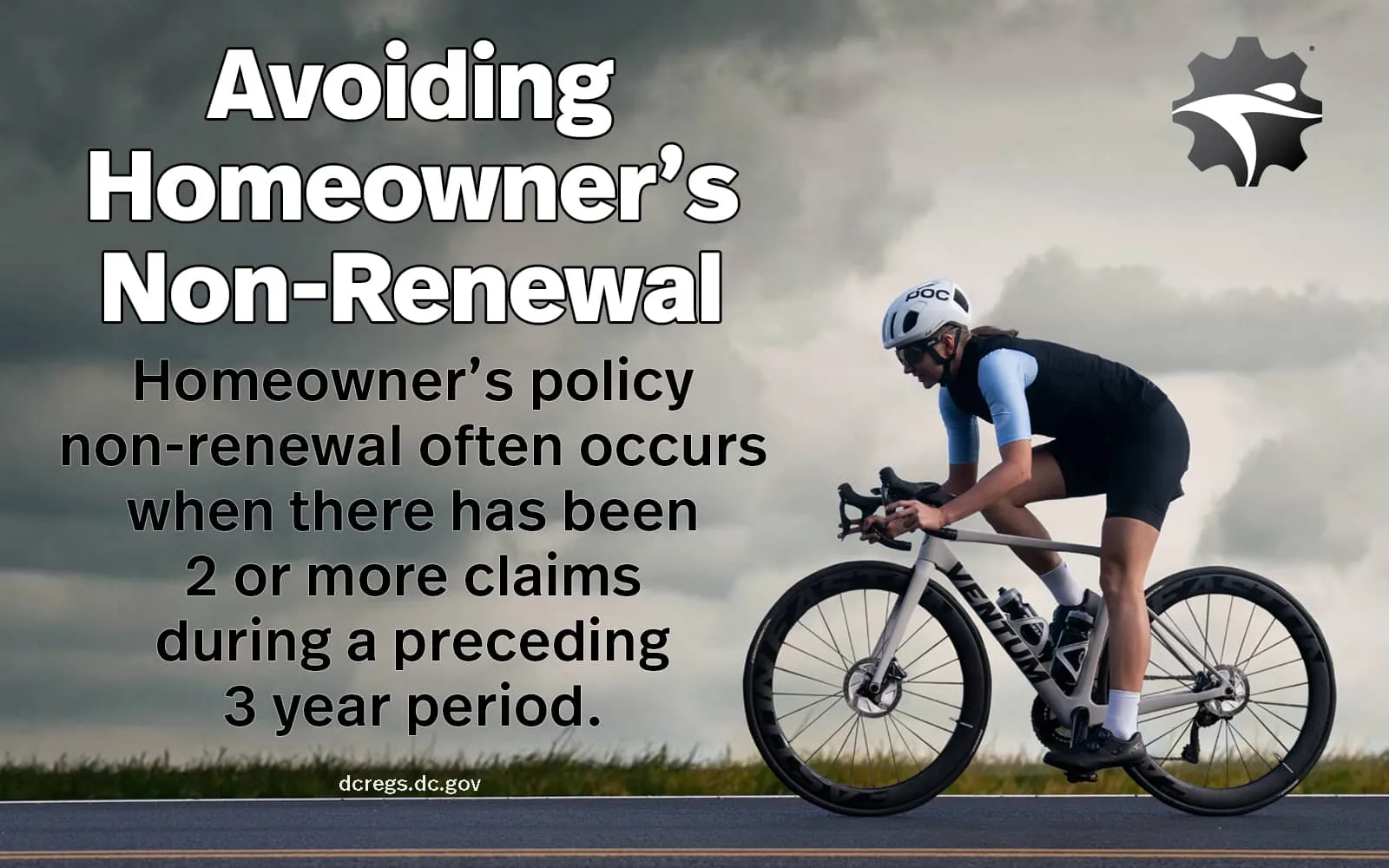

With natural disasters causing carriers to stop selling new homeowner's insurance policies and increasing non-renewals, Cohn recommends that homeowners consider their home insurance as a safeguard against catastrophic losses rather than as coverage for bicycles.

“The non-renewal so-called industry standard when I had my bicycle accident was explained to me by my home insurance claims adjuster executive as, ‘non-renewal when there have been two or more claims within five years. ’However, in more recent years, the standard within the insurance industry has tightened to ‘non-renewal occurring when two or more claims occur within three years.’

Cohn said he calls each new BikeInsure customer to welcome them. Recently, he spoke with a California man whose wife had a similar experience to Cohn's cycling accident.

Her Trek Domane was totaled during a crash, and the couple was told by Farmers Insurance that making a claim could result in eventual cancellation. While Trek’s crash replacement program gave them a 20% discount on a new bike, if they had coverage through BikeInsure, they would have only had to pay the $100 deductible.

Cohn said the husband enrolled his bike, and his wife’s will be, too, when it’s delivered.

BikeInsure It, then Ride It!

BikeInsure thanks Bicycle Retailer and Industry News (BRAIN) for the insightful article regarding the Essential Need for Bicycle and eBike Insurance in the United States.