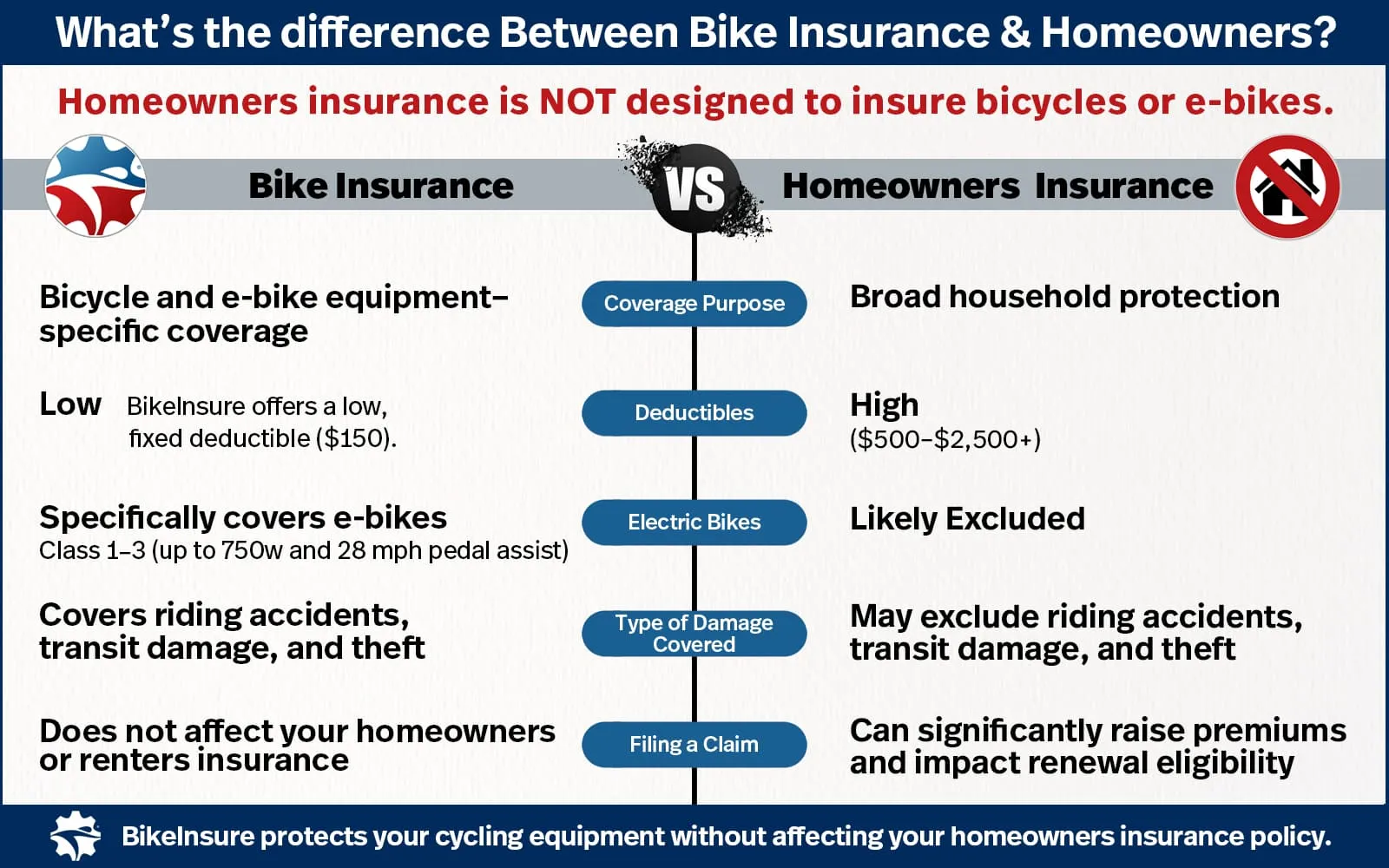

What is the difference between bike insurance and homeowners or renters insurance?

Homeowners and renters insurance are designed to protect your home and major property losses — not high-value bicycles or e-bikes. By contrast, bike insurance — like BikeInsure — is specifically designed to protect against financial loss to bicycles, e-bikes, trikes, and para-adaptive cycles resulting from riding accidents, transit damage, and theft.

Bike insurance is a dedicated policy built specifically to protect cycling equipment from accidental damage and theft.

Here's how they differ:

Coverage purpose

- Homeowners/Renters: Broad household protection

- Bike Insurance: Equipment-specific protection for bicycles and e-bikes

Coverage limits

- Homeowners/Renters: Often low sub-limits for bicycles

- Bike Insurance: You select an Amount of Insurance based on the value of the bike and listed accessories (up to $50,000 with BikeInsure)

Deductibles

- Homeowners/Renters: Commonly $500–$2,500+

- Bike Insurance: Lower, fixed deductible ($150 with BikeInsure)

Type of damage covered

- Homeowners/Renters: May exclude riding accidents, transit damage, racing, or certain theft situations

- Bike Insurance: Covers accidental damage while riding or in transit and offers optional theft protection

Electric bikes

- Homeowners/Renters: Often excluded as motorized vehicles

- Bike Insurance: Specifically designed to cover Class 1–3 e-bikes (up to 750 watts and 28 mph pedal assist)

Impact of filing a claim

- Homeowners/Renters: Claims can raise premiums, affect renewal eligibility, and appear on a CLUE report

- Bike Insurance: Claims are handled separately and do not affect your home insurance

Scheduled property rider

Even when a Scheduled Personal Property endorsement (scheduled insurance rider) is added to a homeowners policy, coverage may still exclude racing, transit damage, and certain theft situations — and the claim still counts against the home policy.

Bottom line:

Bike insurance protects your cycling equipment without risking premium increases or affecting your home insurance claim history, which is why many riders use a separate policy like BikeInsure for their bicycles and e-bikes.